Español

Ecuador

Skills Development / Insurance Solutions Trends

Whole Coverage Planning: Crafting a Safety Net for Clients

January 01, 2025

Estimated Reading Time: 4m

Getty Images

Many consumers view the various types of insurance as unrelated products. Life insurance, health insurance, disability…each one’s viewed in its own separate bubble.

The problem is, this piecemeal approach to insurance can leave gaps in coverage—gaps that may someday create hardship.

A growing number of agents believe it’s their responsibility to help their clients avoid such pitfalls. They’re adopting a more holistic approach, known as whole coverage planning. If you’re not familiar with it, it’s time to learn the basics, so you can get on board.

Addressing the Many Faces of Risk

Whole coverage planning considers the full spectrum of client risk and designs solutions to guard against them all.

It involves crafting a comprehensive safety net for clients, weaving together multiple types of insurance tailored to their needs and situation.

Yes, this holistic approach will naturally lead to more multi‑line clients, but it’s about more than cross‑selling. Whole coverage planning is an overarching philosophy based on serving each client’s best interests.

Components of Whole Coverage Planning

Whole coverage planning typically includes.

- Life Insurance – Provides financial protection for dependents in the event of the policyholder’s death, whether to replace lost income or realize future goals.

- Health Insurance – Covers medical expenses, including doctor visits, hospital stays, prescription drugs and preventive care.

- Disability Insurance ‑ Replaces a portion of income if the policyholder becomes unable to work due to illness or injury. (For family caregivers, alternatives coverages like critical illness may fill this need.)

- Accident Insurance – Covers specific, sometimes temporary risks of injury (such as travel or participation in sports). Also serves as an affordable way to augment life and health insurance limitations.

Many of these are part of your PALIG product portfolio.

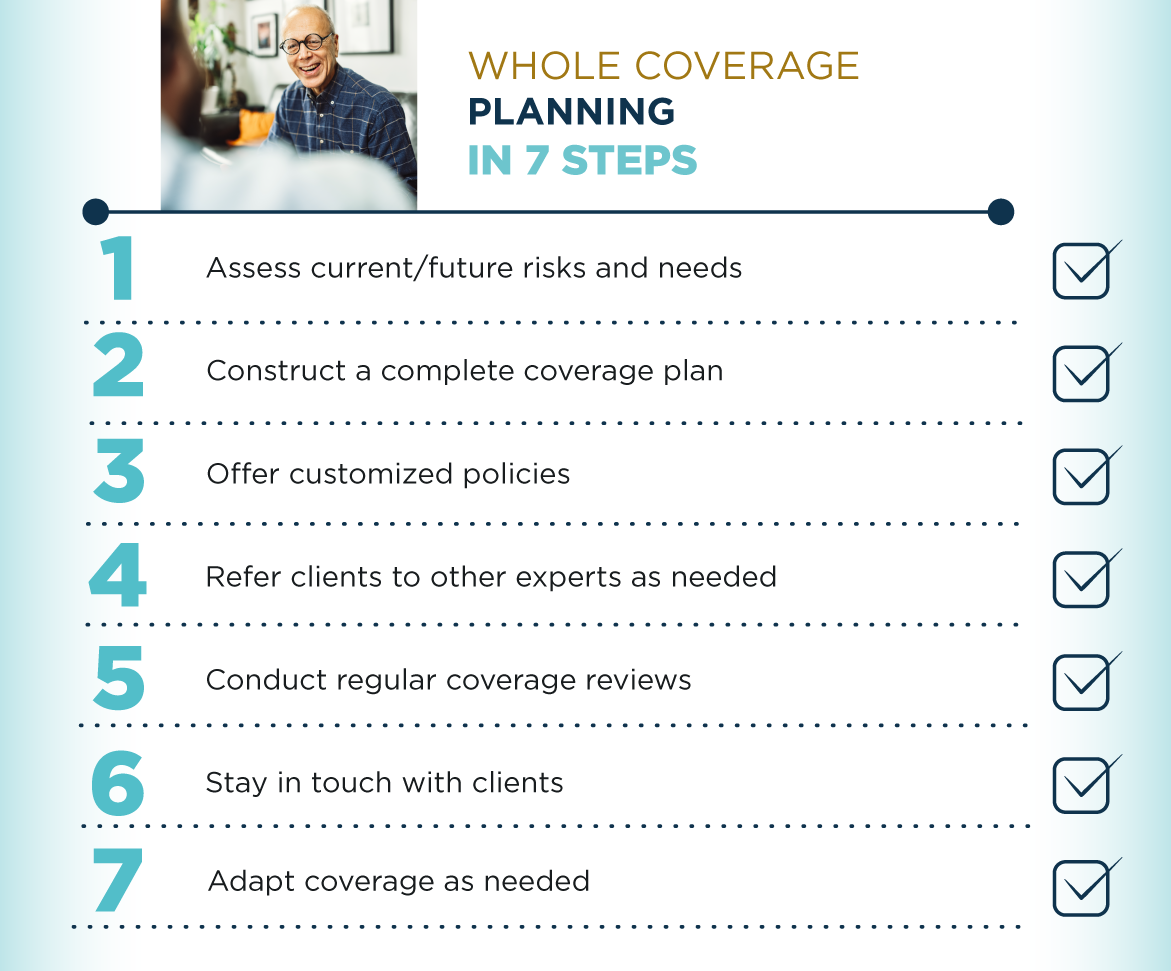

7 Ways to Engage in Whole Coverage Planning

There are a number of ways to incorporate whole coverage planning into your interactions with clients, many which you undoubtedly already do. These include:

- Share Your Holistic Philosophy: Explain why adopting a holistic approach to insurance makes financial sense. Point out the risks of incomplete coverage. Discuss your own insurance journey. Understand that clients may need multiple conversations before embracing the concept.

- Get to Know Your Clients as People: You can’t truly understand a client’s insurance needs without knowing about their lives. Ask about their family, work, goals and worries. Review their existing policies. If you spot a gap in protection, gently bring it to their attention.

- Don’t Close Sales; Build Relationships: A policy sale is not a one‑and‑one, but the chance to build an enduring relationship. Conduct annual policy reviews; touch base on a regular basis. Keep in mind: for clients on a budget, whole coverage planning may need to be implemented in stages—so stay close.

- Keep on Top of Clients’ Life Events: Many major life events—getting married, having a baby—often triggers the need for more insurance protection. For example, if you learn that a client is leaving their job to start a business, that’s an opportunity to explore their individual health insurance needs (and possibly business life insurance, too).

- Think Advisor, Not Producer: Of course, you want to promote the products in your PALIG portfolio and clients should be aware of everything you have to offer. However, when you interpret your primary role as an advisor and educator, more opportunities will present themselves…and the sales will come naturally.

- Keep Track with Technology: Use agency software to track client interactions and set short and long‑term reminders: client birthdays, anniversaries, graduations, etc. Sometimes they lead to new coverage needs. For example, when a client’s child graduates college, send a graduation card—and find out if they now need their own health insurance policy.

- Offer Vetted Referrals : When you promote whole coverage planning, it’s beneficial to have a strong referral network. For example, you don’t sell property casualty insurance, but your colleague specializes in it. Referring clients to expert resources will strengthen your bond and network; while helping you deliver on your holistic promise.

Whole coverage planning is a comprehensive way to approach client risk that benefits them—and benefits you. For more about the PALIG products available to you, .